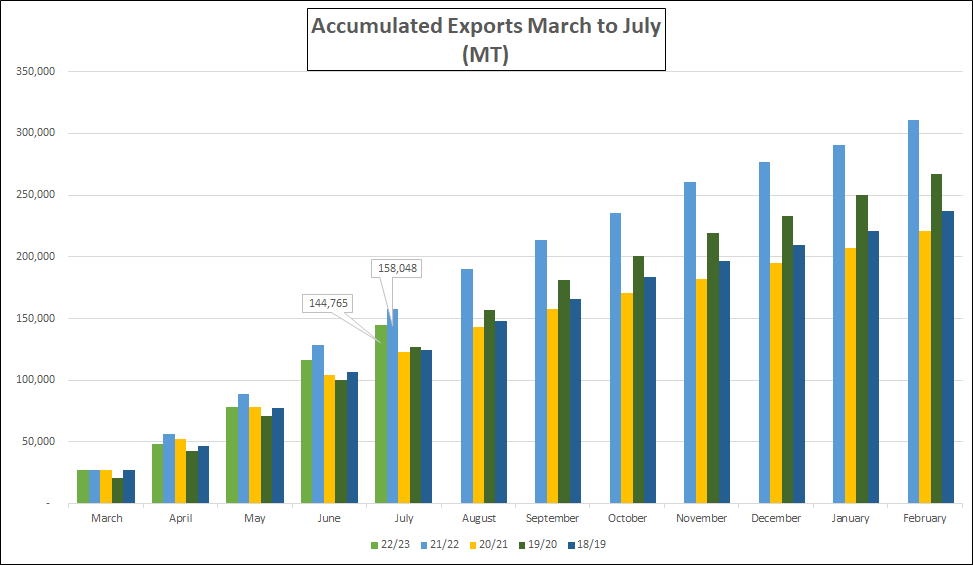

Although accumulated export figures from March to July 2022 are lagging behind the same period in 2021 by 13 K MT, there still is a good chance that by the time we reach Feb 2023 this gap will have narrowed. The only month where shipments between the 2 years was large was April (2022 21 K MT and 2021 29 K MT). Why we believe this? Washed coffee availability is lower this year than last due to a 20% reduction in production y-o-y in the South (Sidamo) region. Washed coffee shipments are skewed to the first half of the shipment year (March to August) and Natural shipments more to the second half (September to February). We believe that despite the high prices traded for Grade 5 coffees, farmers are holding these in their farms and homes as a hedge against inflation and a devaluating local currency. There is a sense that there is a much higher proportion of Natural coffee being retained upcountry this season than last. This is also due to the heavy rain and insecurity that has made transportation to Addis Ababa harder in recent weeks. However, this coffee will eventually flow to Addis for processing and shipment, before the new crop arrives.

Currently, quality of Grade 5 arrivals in Addis is very poor and shippers are accumulating increasing volumes of low quality coffee which they struggle to sell. We expect that from October onwards volumes arriving in Addis will be greater and therefore finding better quality coffees will be easier. Washed coffee longs are beginning to lower their price expectations as they have been holding on to stocks for many months now.

In a world of increasing energy uncertainty the news that a second turbine will start producing electricity at Ethiopia’s new dam will bring some peace of mind to the country’s growing population, for more on this: https://www.bbc.com/news/live/world-africa-61887424?ns_mchannel=social&ns_source=twitter&ns_campaign=bbc_live&ns_linkname=62f4c2c9e4a3c80a9b779e36%26Ethiopia%20dam%27s%20second%20turbine%20starts%20producing%20power%262022-08-11T10%3A57%3A32%2B00%3A00&ns_fee=0&pinned_post_locator=urn:asset:8654f112-73c6-406c-82a0-76446d1dc713&pinned_post_asset_id=62f4c2c9e4a3c80a9b779e36&pinned_post_type=share

Birr 52.21 = USD 1

Have a good weekend.

Leave a Reply

Want to join the discussion?Feel free to contribute!