It is AFCA conference week again, after a 3 year hiatus the East African Coffee Conference is being held in Kigali, great to see so many familiar faces after such a long time!

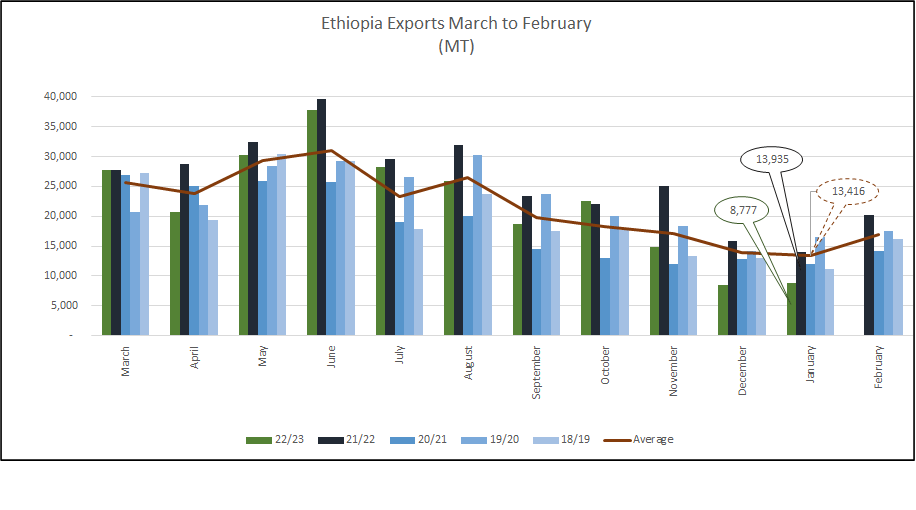

Normally by mid-February Addis Ababa is a hype of activity with mills full of new crop parchment and the first arrivals of natural coffee “fighting” for warehouse space and milling slots. This year the picture could not be more different, warehouses have very little coffee, if there is any at all it is the remaining old crop that will be shipped in the next few weeks. Export registrations continue at very low levels, not even the recent 40 usc/lb rally has been enough to get new crop trading. Something will have to give in the coming months to allow new crop to start flowing:

1. Either the currency devalues

2. The terminal market rallies higher

3. Long holders “throw in the towel”

The other option is for buyers to pay up and accept “never seen before” differential prices… It is difficult to see buyers paying +100 to +150 for Ethiopia Grade 2 coffees while other East African milds from Kenya, Tanzania, Rwanda, Burundi and Uganda are quoted at the AFCA conference at prices between +40 and +65 FOB. Next conference is in Addis Ababa, in a year’s time, it will be interesting to analyse how the 22/23 crop was marketed and what had to give to allow coffee to flow to the export market, my guess is that it will be a combination of the 3 points made above; we could also see some build up of stocks, a normal outcome when downstream players are unhappy with prices.

Birr 53.64 = USD 1

Have a good weekend.