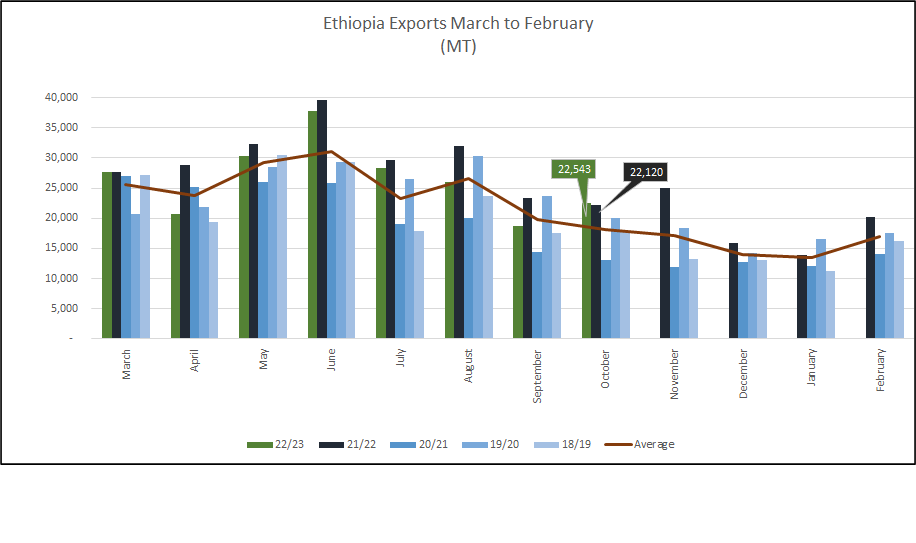

Since March, 2022 monthly shipments have been below 2021 monthly exports, however for October shipments in 2022 were higher (just!) than in 2021. It’s a blip, there is very little coffee around and despite the total collapse in NY over the last few weeks shippers are struggling to deliver on Grade 5 sales made a few months ago at prices around 200 c/lb. Shippers are conscious that if they do not deliver, buyers are only too happy to cancel these contracts buy from the trade of simply buy back hedges, however if the coffee does not exist it cannot be shipped! On the other hand Washed coffee longs cannot find buyers are anywhere close to the prices they want to sell Limu 2 is offered at 300 c/lb and Sidamo 2 at 315 c/lb…

Overall 2022 shipments vs 2021 are down, for the period March to October 2021 exports totalled 235 K MT (11% more than the current year’s 211 K MT) despite the higher prices. The lower exports are, of course, a direct consequence of the lower 21/22 crop, particularly lower in Sidamo region. November shipment should be lower than October, although we expect that shippers will be trying their hardest to fulfil commitments, any unshipped contract will be costly to the exporter.

Out in the coffee growing areas many washing stations remain closed or only operate a few days a week. There is little cash to buy red cherries and prices are between 40 and 60 birr/kg of cherry at farm gate level. Farmers themselves are only selling small quantities of fresh cherries, larger quantities of cherries are being sundried to be sold later; we believe that the rationale is that farmers only sell to get cash for what they need to buy for their current needs. Food inflation is so high (above 40%), farmers believe that holding coffee instead of cash is a better hedge against runaway food prices. Naturals can be held by farmers in their homesteads for months and sold has they need to purchase goods, the hope is that when coffee comes to be sold the price (in local currency) will be higher than today. However, we are sceptical that the government will devalue the Birr substantially and with the C market is freefall, this strategy may not be successful.

There is a problem with current cherries prices in as much as: how much Grade 2 coffee will realistically be sold at a price that will allow the agrabe/exporter to make a return? There will not be many buyers queuing up to pay +150 FOB for their Sidamo 2! With few washing stations operating it is reasonable to expect that Grade 4 and 5 will be produced in higher proportions in 22/23. Since Naturals stay with farmers for longer before being sold to middlemen, it is feasible that farmers’ price for Naturals will be more reflective of the international market price. There is a time lag for overseas buyers’ price ideas to move back the supply chain to the farmgate, however by January the “new price reality” will have sunk in. In January a very high proportion of Naturals will still be in the hands of farmers therefore it will be the farmers that will have to accept much lower prices for the coffee they are currently picking than what they achieved last crop.

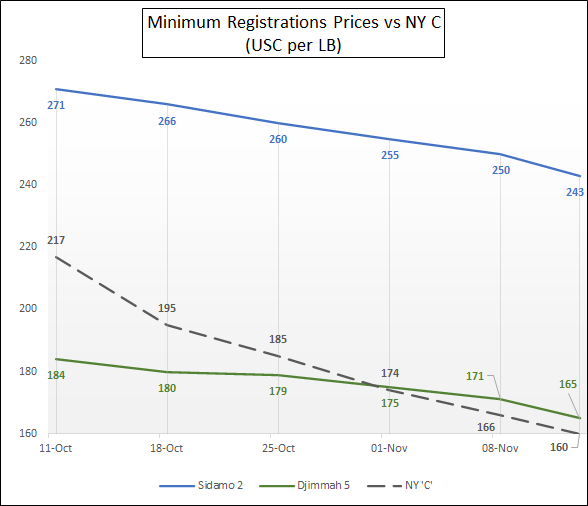

Minimum registration prices have been decreasing over the last few weeks however continue too high to attract any business:

In any event there is very little coffee around, quality of samples that we have been seeing in recent weeks is very poor, there is coffee in shippers’ warehouses however Djimmah stocks have been badly affected by humidity, furthermore, for the past few weeks insecurity has stopped movement of coffee from Wellega (Lekempti) to Addis. Washed Grade 2 coffee stocks are immobilised by the lack of interest from overseas buyers at the offered prices, over 300 c/lb…

Trading is at a complete standstill, the internal market will command the best prices for exporters’ stocks and being less quality orientated can absorb the currently available Grade 5s.

https://www.coffeeithaka.com/wp-content/uploads/2022/11/Coffee-sketch.jpg612474Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2022-11-18 13:03:542022-11-18 18:04:06Harvest is not going so smoothly

The Harvest is well and truly underway! Washing stations are now open throughout the coffee growing regions. However, many remain closed or operating well below capacity (only opening a few days a week). Lack of financing and high prices are the reasons for this. Cherry prices are all over the place, in Guji prices are around 40 Birr per kg cherry, in Limu we hear 52 Birr per kg cherry and in Yirgacheffe price are as high as 60 Birr per kg cherry. To make commercial sense, washing stations should be buying below 40 Birr per kg, this explains why many shippers are not financing cherry buying, preferring to take their chances at the ECX or buying parchment directly from agrabes once the coffee is ready for milling. If farmers are not able to sell cherries they will dry them on their farms and process Naturals which they will sell later. If more washing stations do not open in late November and December in the Southern regions we shall see a smaller proportion of Washed coffees viz a viz Naturals. More Sidamo 4 less Sidamo 2! Size and quality wise we continue to be optimistic, weather continues to be favourable for harvesting and primary processing.

Current crop offers are well above where they should be (above 300 usc/lb for Sidamo grade 2 and above 185 usc/lb for Djimmah 5), even minimum registration prices are nonsensical:

Sidamo 2 250 usc/lb

Djimmah 5 171 usc/lb

Trading is at a standstill, prices are to high and quality is very poor. Prices in the internal market have decreased but remain above export prices and are therefore increasing quantities of coffee are finding their way to the “mercato”.

While on the one hand we are increasingly optimistic that the Ethiopian conflict that has been raging for the past 2 years has a chance to finally come to a resolution, when it come to the coffee crop, the situation is rather dire. Many washing stations in areas that produce some of the country’s best coffee are not opening, mostly because of lack of financing and resistance from farmers to sell at the current market prices after the crop started being marketed at much higher levels only 4 weeks ago. This places a big question mark on the availability of washed coffees in the coming months as farmers that may be unhappy with fresh cherry prices will simply dry these and sell naturals. This option affords farmers the option to sell their produce at a later date but reduces the availability of washed coffees for 2022/23 crop. Many shippers that advanced cash to agrabes last season are not doing so this season since their experience was indeed very bitter having been delivered poor quality at inflated prices. Furthermore, while during the 21/22 harvest terminal market prices headed North this year the opposite is true; the terminal market continues its relentless drive downwards shelshocking stakeholders all along the supply chain. If cherry prices return to more reasonable levels as they appear to be doing (we understand that in parts of Guji prices are at 40 Birr/kg cherry) then it will be farmers that absorb the lower prices rather than shippers and middlemen as it has been in the last few months.

Meanwhile we continue to struggle to get coffee shipped, lack of containers and vessels calling Djibouti the same old reasons for delays and more delays. On a more positive note, quality of coffee arriving in Addis from Wellega and other Grade 5 regions is improving as the weather is drier.