All

Buying of cherries is ongoing in all coffee growing regions of Ethiopia. A little alarmingly prices for kg of cherry are between 20 and 25 Birr per kg cherry depending on the region; at current terminal levels differentials would start at + 3 digits…

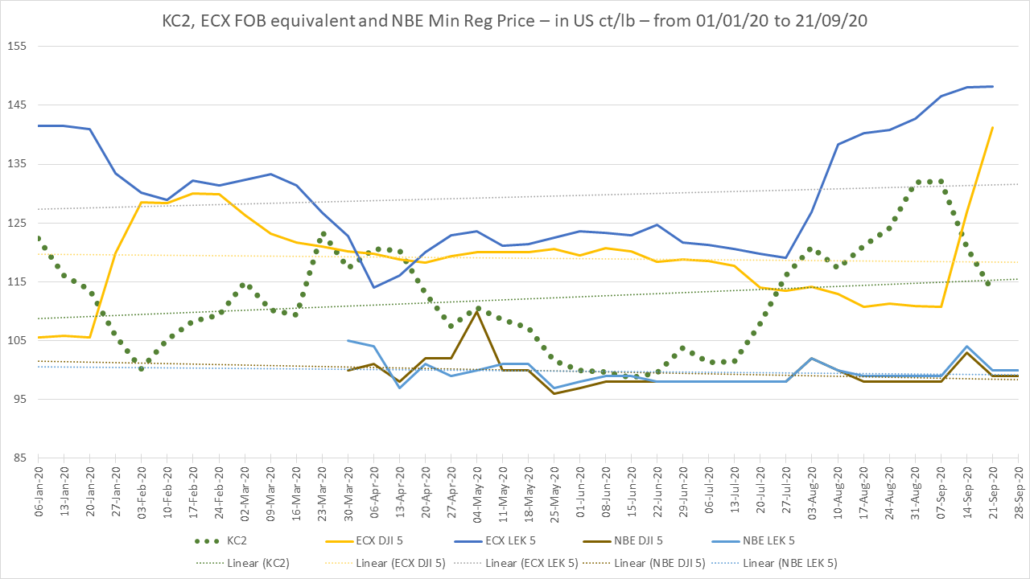

Demand for Naturals at ECX continues to outstrip supply; one the reasons for this is that there seem to be new players getting into the coffee export business since sesame seeds and other crops are less attractive than in previous years and importers need access to hard currency that they can only get from being in the export business. These new players are upsetting the more established shippers that are struggling to fulfil shorts and have asked for Coffee and Tea Authority support but it is hard to see what the regulators can do since production this year is down and quality poor.

Weather conditions continue favourable in most areas and the harvest is progressing well.

Birr 37.50 to the USD

Have a great weekend.