The relentless decline in terminal prices has brought whatever small interest there was to a holt. Minimum Registration Prices for Grade 5 coffees are around level NY so there are no buyers. Washed qualities are also over priced at over 280 c/lb for Yirgacheffe 2 and Sidamo 2 with Limu 2 at 225 c/lb FOB, particularly in light of decreasing differentials for other Milds from around the globe at the same time as NY collapses.

Weather wise the rain continues to affect transportation from upcountry to Addis, the rain is positive for the next crop but is impacting current shipments negatively.

https://www.coffeeithaka.com/wp-content/uploads/2023/06/cupping-pic.png869752Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2023-06-30 16:35:132023-06-30 16:35:14Minimum Registration Prices back in play

May inflation rate = 30.8 % which might sound like a high rate of inflation however it’s the lowest monthly rate since 2021 and a decrease from 33.5% in April 2023. Unfortunately that is where the good news stops! The problems that have been plaguing the coffee business in Ethiopia we have been mentioning time and time again in recent weeks persist:

Rain and humidity

Poor quality, particularly in Grade 5 coffees from the Wellega (Lekempti) and Djimmah areas

Delays in internal movement of coffee from growing areas to Addis, a consequence of the heavy rain

Pressure to export piled on by the Government

Low Export registrations

Shippers are so delayed with their shipments, however it is a general situation, we are not able to single out one or two as worse or better than others, everyone is late and quality is very poor.

We have had conversations with a few shippers in Athens this week and the general feeling is that quality will not improve this crop. The general situation for coffee in Ethiopia is quite depressing with all stakeholders unhappy with the coffee business and struggling to keep above water. Things can only get better, but will they?

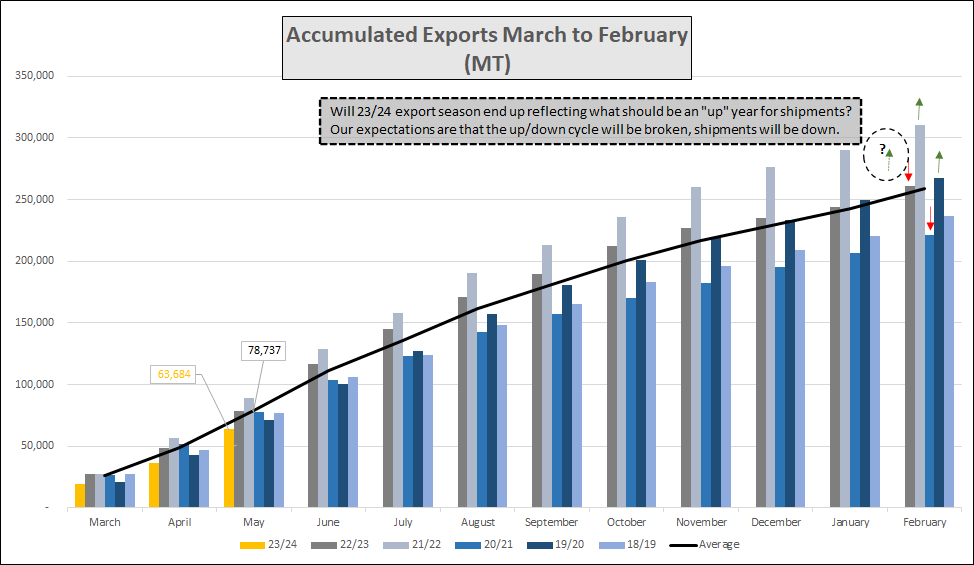

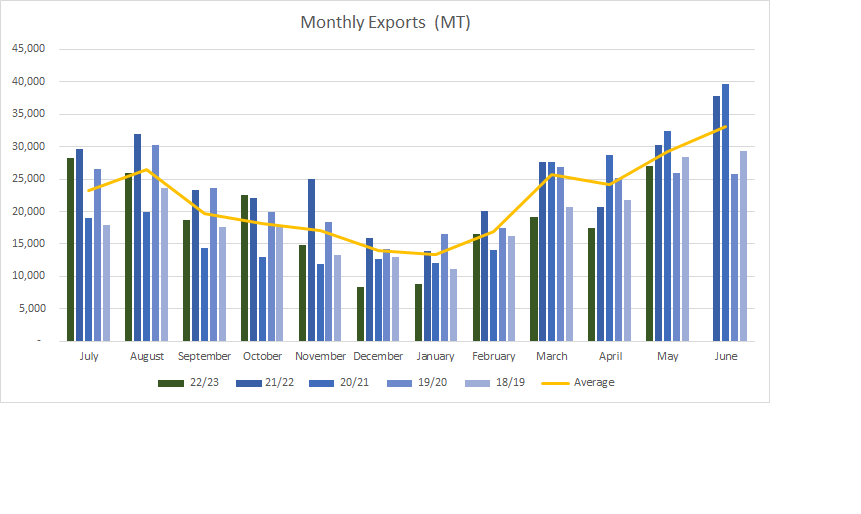

We are early on in the shipment season, however we projecting that exports for teh coming months will be below potential, the last 3 months (March to May) exports reached 68 K MT well below the 5 year average of 78 K MT and last year’s at May shipments.

https://www.coffeeithaka.com/wp-content/uploads/2023/06/bags-1.png34565184Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2023-06-23 15:00:482023-06-23 15:00:54Inflation decreases in May

Shipments in May increased by 10 k MT on the April figure. At 27 k MT the exports for May are much improved on the April exports however remain 2k MT below the average of May shipments for the previous 5 years. When the Coffee & Tea Authority publishes its annual export figure it is very likely that the 22/23 cycle will be the lowest for the past 5 years.

In a bid to accelerate shipments and push exporters to ship, the Ministry of Trade is introducing a new 15% Tax on coffee that is held for over 12 months unshipped. Additionally, there will be penalties for “hoarding” coffee rather than shipping. This move is the latest attempt by the Government to increase exports and attract foreign exchange to sure up the local currency. For the last 6 months+ coffee shipments have fallen below expectations and potential, due to poor quality (of Natural Grade 5 Coffee) and high asking prices (particularly for Washed Coffee). Will this latest Government intervention have the desired effect? We somehow see this as a desperate move that may not have any tangible results, taxes do not improve quality!

May shipments will be published soon, our feeling is that these will once again disappoint; stocks in Addis continue high, warehouses are full of coffee that is stuck due to poor quality or priced out of the market. Coffee is not moving from upcountry to Addis due to the heavy rain that has been battering the country since March. This is a very atypical season, this time of the year is normally peak season for processing and shipping, however this year is far from normal!