Shippers continue to offer, however a combination of lower terminal market, higher minimum registration prices and buyers having “filled their boots” when NY rallied a couple of weeks’ ago have resulted in less business being concluded. Quality concerns are an ongoing issue, both in Naturals and Washed coffee qualities. Weather continues wet, normal for this time of the year.

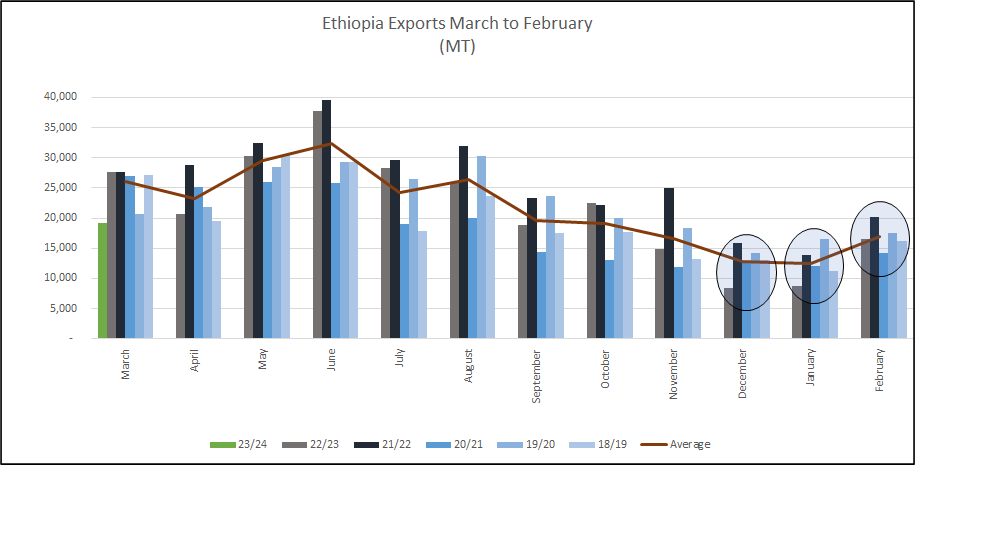

As we approach the end of the month we look forward to analysing the shipment figure for April, although this show a marked increase on previous months we suspect that full potential will not have been reached. Quality issues and resistance to lower prices (or prices lower than farmer expectations) have resulted in retention at farmgate level. Coffee is flowing much better than a few weeks ago however, it is not a flood!

In other news, violence returned to Amhara region this week with the killing of a local leader: https://www.bbc.com/news/live/world-africa-65355011?ns_mchannel=social&ns_source=twitter&ns_campaign=bbc_live&ns_linkname=644b4c3b1719d30b241ce099%26Ethiopia%27s%20Amhara%20ruling%20party%20official%20shot%20dead%262023-04-28T04%3A40%3A13.660Z&ns_fee=0&pinned_post_locator=urn:asset:b43f0506-21da-4ba5-a4b4-45e8db7fad21&pinned_post_asset_id=644b4c3b1719d30b241ce099&pinned_post_type=share

There seems to have been some movement on the Ethiopian side of the argument regarding the dispute with Egypt over damming the Nile: https://www.bbc.com/news/live/world-africa-65355011?ns_mchannel=social&ns_source=twitter&ns_campaign=bbc_live&ns_linkname=644a1a0cbb343d77c4990f55%26Ethiopia%20says%20ready%20to%20resume%20Nile%20dam%20negotiations%262023-04-27T07%3A01%3A48.417Z&ns_fee=0&pinned_post_locator=urn:asset:8ffac229-ead9-4b1b-9a3d-3c3211594947&pinned_post_asset_id=644a1a0cbb343d77c4990f55&pinned_post_type=share

Forex 54.14 = USD 1

Have a good weekend