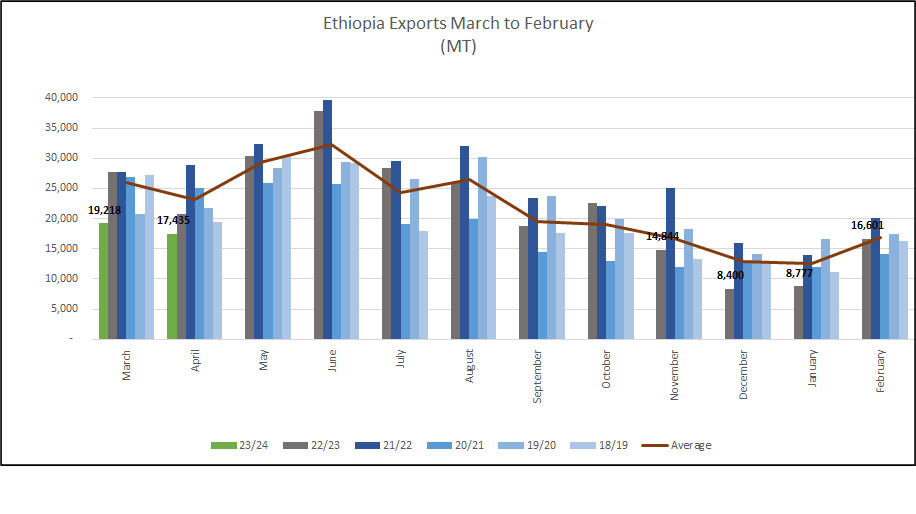

The weather continues to be humid and is getting colder as “winter” approaches. Rain stops coffee from drying or remaining at optimal moisture levels, and makes roads impassable. Quality concerns are ongoing with many samples rejected for earthy, musty cups. Meanwhile shipments, while not completely at a standstill, are much lower than what they should be; particularly considering the sales done when NY rallied in February and again in April. Indeed as the NY rallied in late February to 190+ and then again in April to 200+ shippers sold, however contracts remain unshipped as intrinsic quality is lacking with cup defects that originate in poor preparation and wet weather conditions.

Natural stocks held in warehouses in Addis remain high, coffee is stuck, not moving out to be exported. The reason remains the same, poor quality, buyers are not approving Pre-Shipment Samples and since quality issues are widespread (the whole crop is compromised) the problem is not easily solved!

There were fresh rumours of devaluation this week however as of today the Birr Official Rate remains at roughly 50% the Black Market Rate as follows:

Birr 54.28 = USD 1

Have a good weekend.