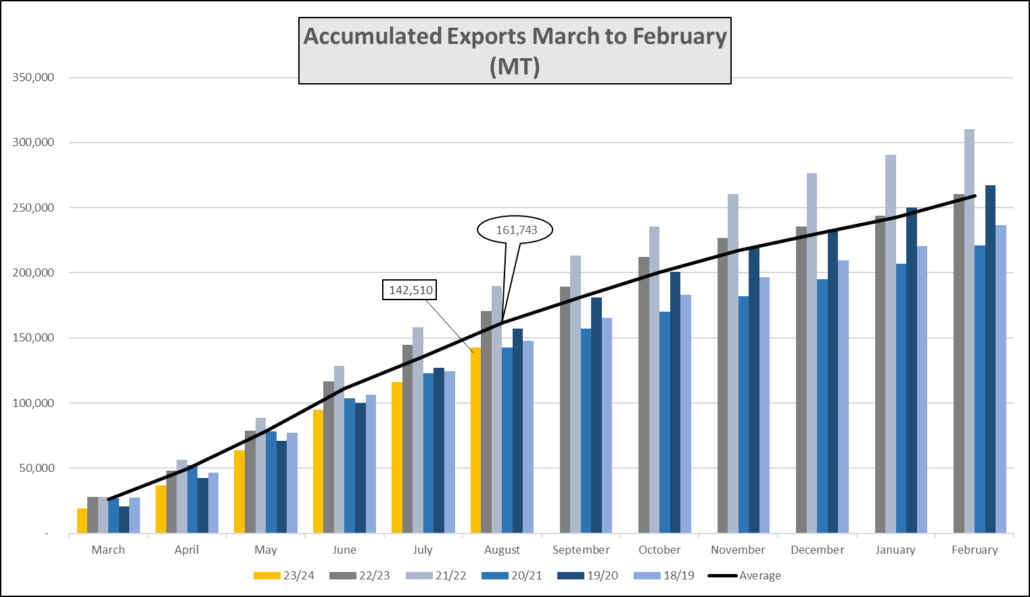

Shipments for August reached 26 k MT, which is the average for the last 5 years. However the 6 month exports March to September 2023 is still 19 K MT below the period’s average of 161,743 MT. We are now half way between the shipment period February to March, and it looks like we are going to struggle to reach 4 M bags for the the full year. Plenty of coffee remains upcountry, agrabes are still holding substantial volumes of parchment and farmers still hold above average dried cherry inventories; export volumes can only recover if these stocks are bought and exported by shippers. However, banks are reluctant to further finance non performing shippers and quality of the coffee that remains in country is generally poor. Prices in the internal market have dropped as there are more sellers than buyers at present. Paradoxically, Minimum Registration Prices for export contracts have remained unchanged for several weeks, so overseas buyers cannot even be tempted by low prices.

Ethiopia announced this week that the GERD dam has reached a new milestone: https://www.bbc.com/news/world-africa-66771155

Birr 54.14 = USD 1

Have a good weekend.

Leave a Reply

Want to join the discussion?Feel free to contribute!