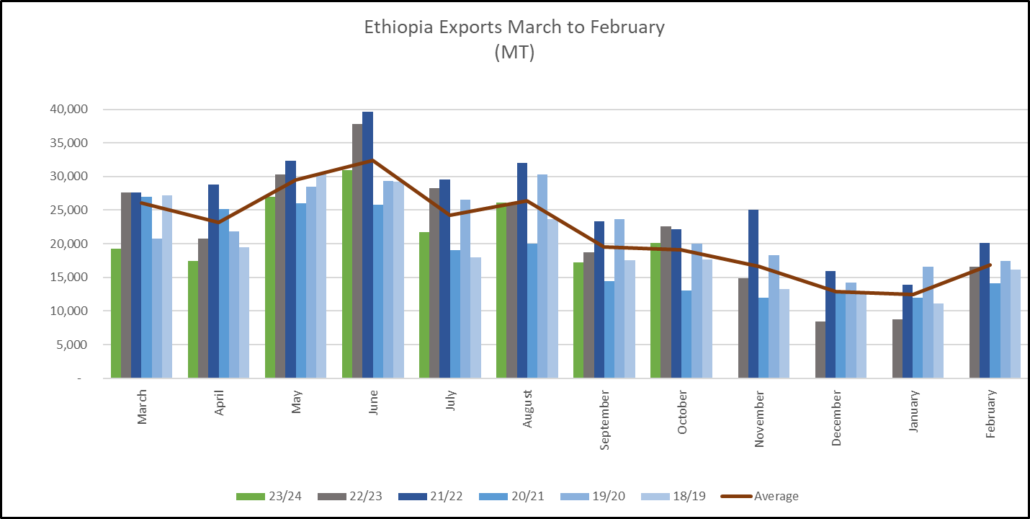

Exports for October topped 20 K MT; Shippers started “throwing in the towel” under pressure from Coffee & Tea Authority penalties, seeing the New Crop on the trees ready to be picked and steady prices. November shipments should continue this recent improved performance aided by the recent buoyant NY terminal market which as come just in time to help clear warehouses waiting to receive New Crop coffee. These strong October shipment figures followed on from very robust September shipments, however 22/23 exports are lagging behind expectations and even if the coming months register above average shipments by the time New Crop coffees come to market (March 2024) shipments will still be lower than expected.

Washing stations in the South have started receiving cherries, prices are 25 Birr/kg. It really seems that thus far stakeholders have taken heed of last years pricing chaos and have become much more disciplined (last year cherry prices in the South were between twice and 3 times current prices). There is also much less cash available in the field for cherry buying, leading to less competition which in the past has fueled pricing hikes.

Currently there is not much interest for new crop offers, it appears that roasters are waiting for lower prices and/or clarity on demand. Trade buyers are put off by the lack of carry in the market and high (even if stable) interest rates.

In other news, one year on from the peace deal between Tigray rebels and the Government, the BBC reports on the situation in the North of the country: https://www.bbc.com/news/av/world-africa-67290495

Birr 55.63 = USD 1

Have a good weekend.

Leave a Reply

Want to join the discussion?Feel free to contribute!