All

It seems that the new Government in Ethiopia has as a priority to deal with the crisis in Tigray, launching a large scale military offensive this week. For the BBC’s take on the issue please follow the link: https://www.bbc.com/news/world-africa-58869970

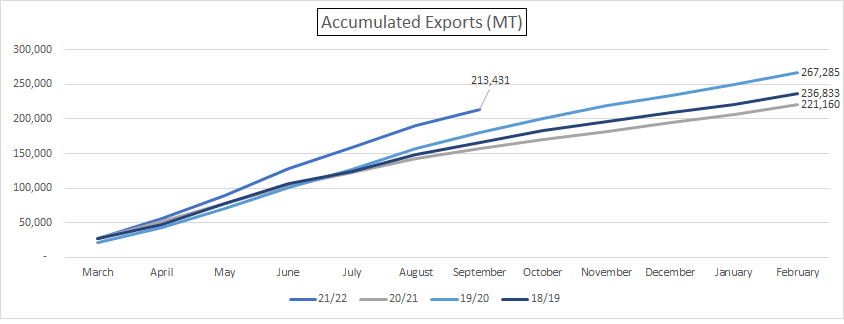

Meanwhile the September Export numbers show a decline in shipments vs August, as expected, and this reducing seasonal trend is likely to continue for the coming 3 months. Shipments have been heavily skewed towards the first half of the shipment year so the pace of sales for the period Sep to Feb is also likely to decrease more than usual. Warehouses and processing mills are looking very empty, only dwelling stocks remain in Addis unprocessed and unsold, recent spikes in the terminal market having flushed out much of the remaining stocks.

On the logistics front, finding containers to stuff is getting harder, whenever a vessel leaves Djibouti it seems to have dozen of our containers since there are so few calling Djibouti. Our shipments pile up at the port until a vessel finally comes and then it all loads! Timelines from PSS approval to FOB are getting longer all the time, not even the reduction in shipments has helped. With the economy stagnating because of the fighting, imports are lower and consequently the number of available containers is also reduced.

New crop has started in a few areas like Benchi Maji. Limu area is expected to start second half October. Cherry prices are all over the place ranging from 20 to 30 Birr/kg. However we only expect to get a meaningful cherry price level once the harvest gets underway in earnest, in November.

Birr 46.66 = USD 1

Have a good weekend.

Leave a Reply

Want to join the discussion?Feel free to contribute!