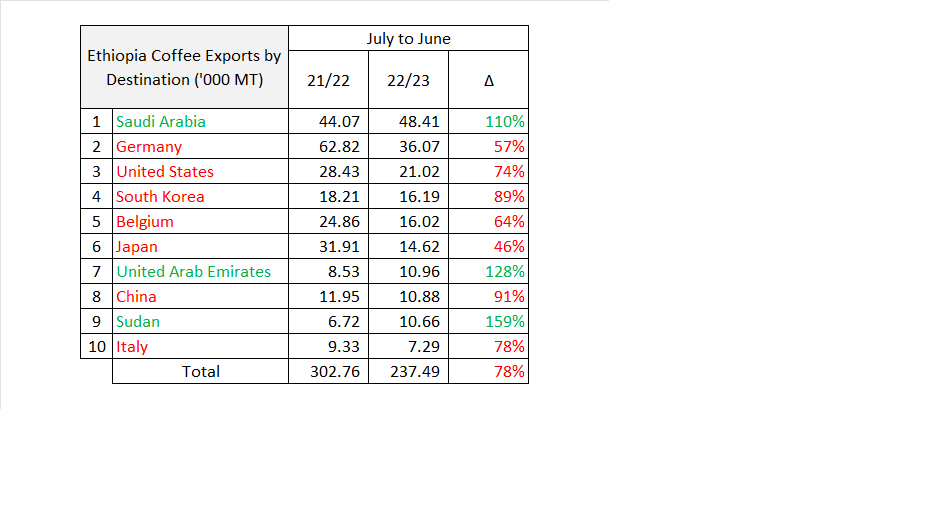

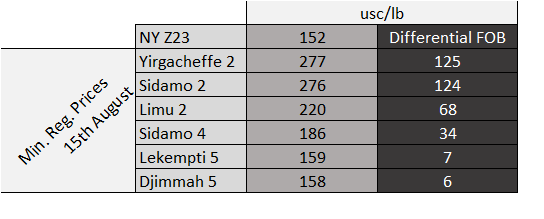

The Coffee and Tea Authority decreased Minimum Registration Prices by 3 cents, however Grade 5 FOB prices remain at a premium to NY. As a means of getting around this impediment to trade Under Grade (UG) sales are being registered at the current Min Reg Price of 133 c/lb.

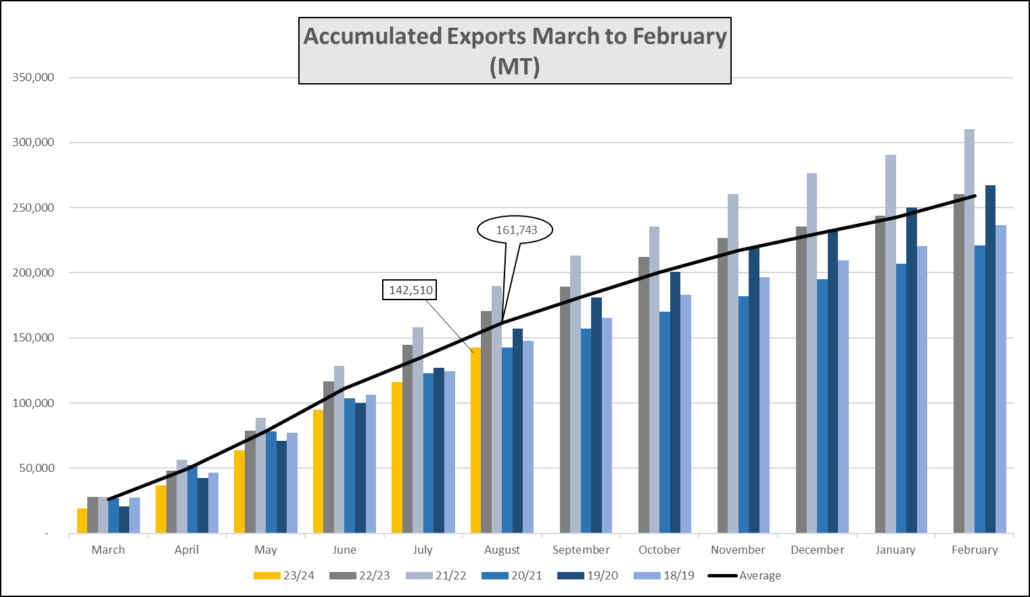

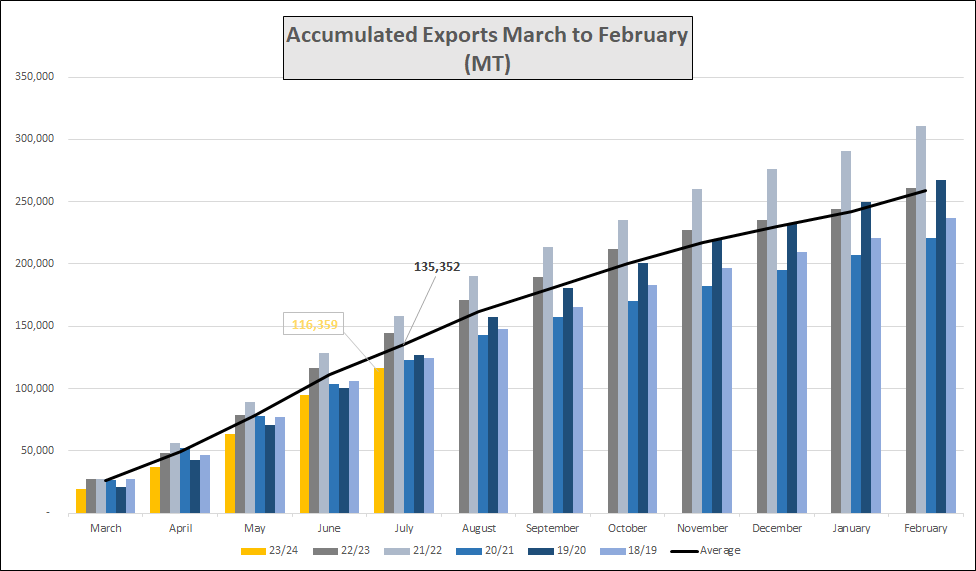

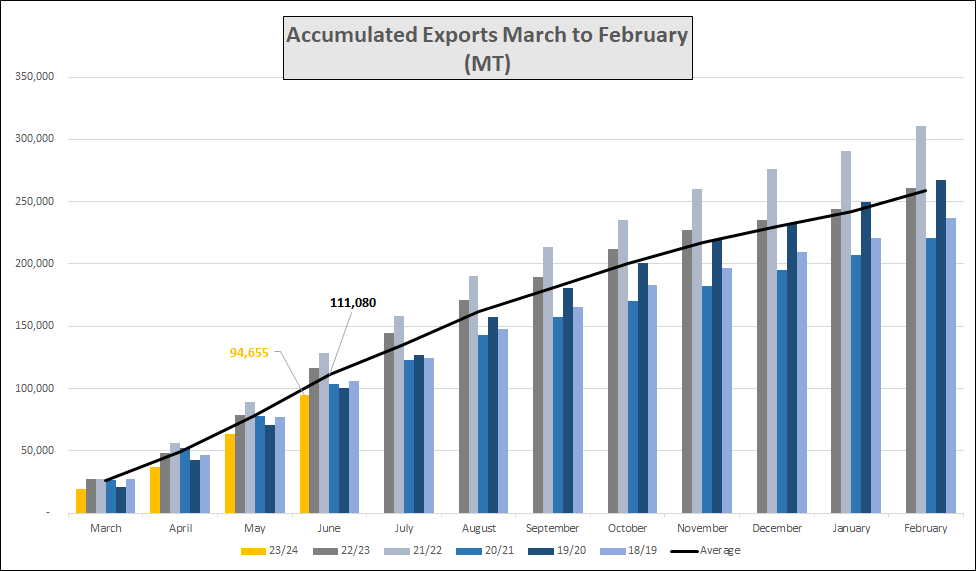

New crop harvesting continues without any hiccups, weather remains favourable and prices much more in line with international market prices. The security situation in several regions of the country seems to have improved in recent weeks, this will greatly help farmers as the coffee harvest gathers pace. In Tepi the first samples will be available as early as next week.

In other news, a UN-backed inquiry into abuses committed in Ethiopia will end its work next week after member countries chose not to renew its mandate. Furthermore, the US Government resumed distributing much needed food aid, for more on this please follow the link: https://www.bbc.com/news/world/africa?ns_mchannel=social&ns_source=twitter&ns_campaign=bbc_live&ns_linkname=651fb4def34eee40bb92a8fe%26US%20resumes%20food%20aid%20to%20refugees%20in%20Ethiopia%262023-10-06T08%3A58%3A57.862Z&ns_fee=0&pinned_post_locator=urn:asset:9a9af04e-4ecb-4f43-a189-1da65001c87c&pinned_post_asset_id=651fb4def34eee40bb92a8fe&pinned_post_type=share

Birr 55.28 = USD 1

Have a good weekend