For the first time ever there is no Lekempti coffee and only 150MT of Djimmah coffee in ECX warehouses waiting to be sold, in total only 500 MT of Naturals are waiting to be sold at ECX warehouses. The reason is clear, agrabes will not bring coffee to the market while price ceilings are in place, this impasse has to be resolved soon or the pace of shipments will continue at the very low levels of recent months or fall even further. Furthermore, the National Bank of Ethiopia has stopped allowing registration of 2019/2020 crop coffee which had lower Minimum Registration prices than 2020/21 crop coffee so unless the NY market rallies strongly we see registrations for Washed coffees also stopping since there is little appetite for Sidamo 2 or Yirgacheffe 2 at around +100 FOB.

The Government forces continued their offensive against the leadership of Tigray region forces adding more victories to the initial taking control of the northern region territory. Tensions with neighbouring Sudan continue but little fallout to report.

https://www.coffeeithaka.com/wp-content/uploads/2020/08/IMG_4084-Slide.jpg925694Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2021-01-15 18:03:192021-01-18 15:54:29Standstill in the internal and external markets

Happy New Year, may 2021 be a little more predictable than 2020!

In attempting to address Exporters’ sourcing problems the Coffee and Tea Authority (C&TA) has allowed shippers to sell coffee between themselves increasing liquidity in the internal market, we see this as a positive move allowing those exporters that have coffee but no export market to offload excess stock and free cash while permitting short shippers to tap into an alternative supply to fulfil commitments. Meanwhile at ECX, volumes on offer are smaller when compared to this time in previous years. Traders are still upset with the C&TA meddling with prices, in particular capping the maximum price coffees can fetch at ECX. ECX Warehouse stock levels remain low when we would expect these to be building up. The problem with delayed shipments continues with no end in sight… A further consequence of diminished activity internally is a reduction in offers from shippers, particularly in lower grades (Grades 4 and 5).

National Bank of Ethiopia Minimum Registration prices for Exports (also set by the C&TA) remain too high for Washed Qualities buyers, bid levels are around 30 cents below offered levels.

USD 1 = Birr 39.20

Have a good working week, and Merry Christmas to our Ethiopian friends.

The Coffee and Tea Authority is continuing with their ECX Maximum price policy, however price limits have been increased so there is less tension between collectors (Agrabes) and the C&TA. Export Registrations of Washed Coffee are very disappointing so the pressure is on for the C&TA to reduce minimum registration prices for grade 2 coffees from the South. Volumes at ECX are still reduced and shippers continue to struggle to cover shorts established long ago and in many instances rolled over. Some of the larger exporters have stopped offering for nearby shipment not wanting to increase their very short positions. Several donor organisations are limiting their support to Ethiopia over concerns of Government actions in the North of the country so we expect that pressure is mounting on Exporters bring in foreign currency to alleviate the shortfall in overseas remittances from international partners.

Unknown assailants attacked a village in North Western Ethiopia and it seems that a massacre has taken place. This comes the day after the Prime Minister toured the area, therefore it is an obvious conclusion that this occurrence is linked to the PM visit and the recent fighting in Tigray region. It always was a real concern that having stabilised the main cities in Tigray, the security forces would be facing guerrilla warfare and terror attacks. We expect that these strikes towards civilians will only strengthen Central Government resolve to subdue Tigray fighters. Peace in Ethiopia is not assured in the near term.

The harvest is entering its closing stages, cherry prices range between 20 and 27 Birr per kg, a considerable variation in prices and depending on the area. In Yirgacheffe areas competition is strong, whereas in other areas coffee is starting to dwindle and there is less demand.

Birr 38.94 to the USD

Have a nice weekend, stay safe over the festive period.

https://www.coffeeithaka.com/wp-content/uploads/2020/08/ithakaDSC00741.jpg18001200Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2020-12-24 15:42:252020-12-24 15:42:27Some tensions ease, others not so much

In early 2020 the Coffee and Tea Authority introduced Minimum Registration Prices for export coffee, now we have Maximum Sales Prices at ECX! Consequently Agrabes stopped selling coffee at ECX! It is easy to understand why, one day you are selling at 1,900 and the next the price is capped at 1,300! In recent weeks ECX prices have been driven upwards on tight supply and huge demand, both for Export and by Internal Demand, Exporters complain that the ECX price is too high but I am not sure that capping the price is going to help exporters…

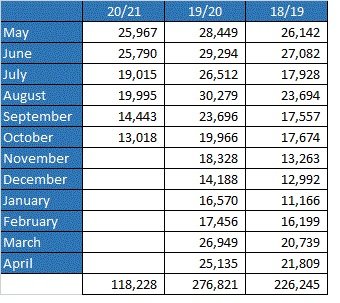

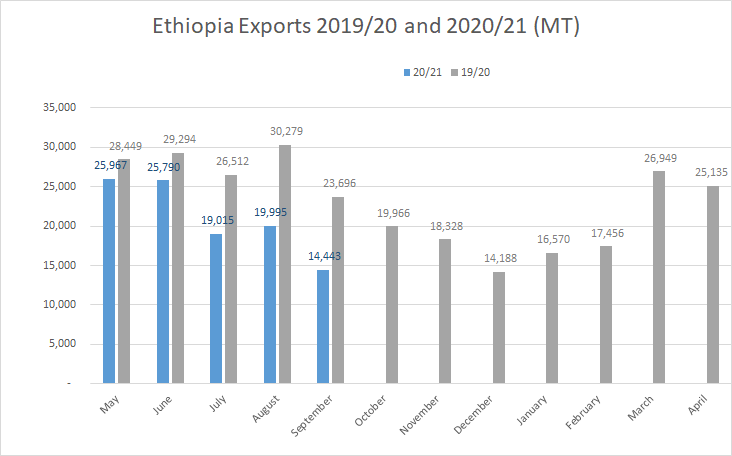

Exports in November decreased as is normal for this time of the year, however the pace of sales is much lower viz a viz 19/20; the period May to November 2020 is 46 k MT behind the same period May to November 2019:

20/21

19/20

May

25,967

28,449

June

25,790

29,294

July

19,015

26,512

August

19,995

30,279

September

14,443

23,696

October

13,018

19,966

November

11,964

18,328

(Export figures in MT)

Meanwhile registered sales of Washed New Crop 2020/21, for shipment first quarter 2021, is very low as a direct consequence of the high Min Prices for Sidamo and Yirgacheffe, these grades cannot be registered below 220 c/lb; Limu seems quite reasonable at around +50 FOB equivalent. Steady business for Lekempti and other Naturals for both current and new crop this week.

Ongoing limited supply to ECX with Djimmah 5 trading at around 175 c/lb FOB equivalent; FOB buyers are bidding around 95 c/lb and the local market is paying 350 c/lb, so it is no surprise that shippers do not have anything to sell and that coffee is not arriving at ECX warehouses. Any coffee that is around is finding it’s way to the local market illegally but the incentive is too great. Volumes of Naturals at ECX are pitiful, yesterday 166 MT of Sundried (all grades) were offered; we do not expect to see any meaningful quantities of Djimmah type until February and Lekempti/Sidamo (Natural) until March so local tightness is likely to continue for a few more weeks.

Minimum registration prices for New Crop Sidamo 2 is over 220 c/lb FOB, which is too rich for most standard Sidamo 2 buyers. The Coffee and Tea Authority (CTA) does not seem to understand that there are different qualities of Sidamo 2 and that most will only find a market if traded at much lower levels; in time we believe that this minimum registration price will be reviewed to better reflect levels where larger buyers and standard quality is tradable.

Ethiopia appears to be much more peaceful this week although there remains a heavy military presence in Tigray region.

https://www.coffeeithaka.com/wp-content/uploads/2020/09/rachel-clark-_1wChzif1EM-unsplash-scaled.jpg17062560Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2020-12-11 18:05:092020-12-11 18:05:10Not much coffee around

Government forces have taken the main town in Tigray region, Mekelle, however the TPLF leadership have not been arrested which was the main justification for launching the offensive in Tigray. For now the region is stable and not as tense has in the previous month of November. The focus seems to have moved to aiding the displaced population that are in need of food and other basic necessities.

Exports continue to disappoint, during the 6 month May to October 2020 vs same period in 2019 volumes are down by 40 k MT or 25%. If you only look at the last 4 months, the drop is even greater at 34% between 2020 and 2019. This poor pace of shipments is expected to continue until the New Crop starts to be exported which could be early 2021 as the harvest was early and the weather conditions post-harvest favour parchment drying. Quality wise indications are that the crop is good and better than 19/20 quality. Reported cherry prices are still very high, as much as 27 Birr per kg in Yirgacheffe.

https://www.coffeeithaka.com/wp-content/uploads/2020/08/ithakaIMG_3016.jpg15551037Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2020-12-04 16:54:232020-12-04 16:54:25Fighting nearly ends but is it over?

Notwithstanding the conflict in the North of the country Ethiopian Coffee business continues at great pace; the NY market rally has made differentials more attractive and shippers have been able to register some sales in the past few days. At ECX the volumes on offer have increased as the New Crop harvest is in full swing and possibly as a consequence of these more turbulent times that we live in Ethiopia these days. Shippers are very eager to execute their commitments, getting coffee on vessels and be paid. You certainly get the feeling that the conflict is affecting all aspects of Ethiopian life and shippers decisions.

Meanwhile there is very little news from the conflict zones; again rockets from Tigray were fired at Amhara towns. In Addis the Government has arrested scores of influential and prominent Tigray military leaders and other persons, while at the same time freezing bank accounts and assets. An estimated 30,000 civilians have fled Tigray to Sudan to escape the conflict.

So far the pace of shipments is very disappointing, reflecting the poor 19/20 crop, May to Sep 2020 shipments are 33 K MT (25%) lower than same 5 month period in 2019:

https://www.coffeeithaka.com/wp-content/uploads/2020/11/ResizedLogistics-7.png6481152Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2020-11-20 16:40:222020-11-20 16:40:24Better market, more sales and increased volume at ECX

Buying of cherries is ongoing in all coffee growing regions of Ethiopia. A little alarmingly prices for kg of cherry are between 20 and 25 Birr per kg cherry depending on the region; at current terminal levels differentials would start at + 3 digits…

Demand for Naturals at ECX continues to outstrip supply; one the reasons for this is that there seem to be new players getting into the coffee export business since sesame seeds and other crops are less attractive than in previous years and importers need access to hard currency that they can only get from being in the export business. These new players are upsetting the more established shippers that are struggling to fulfil shorts and have asked for Coffee and Tea Authority support but it is hard to see what the regulators can do since production this year is down and quality poor.

Weather conditions continue favourable in most areas and the harvest is progressing well.

The crop has started to be picked and collected in nearly all producing areas of the country, only the higher growing areas like Yrgacheffe are yet to start. Our initial thoughts of decent quantity and quality remain unchanged, below we list the cherry prices that we have heard are being paid by washing station owners in Birr per kg cherry:

Guji 18-19

Sidamo 15-16

Limu 15

Kaffa 13

These prices are in line with prices paid to farmers last season, however as mentioned the crop is expected larger so it would not be unreasonable to have expected lower prices to reflect the larger crop, however the flow is small presently and only a few Washing Stations are working; as the flow increases and supply increases, if it outstrips Washing capacity we could see prices stabilise or even drop; on the other hand if demand from Washing Stations increases and competition to attract cherry intensifies then the price will go up. It is still a little early to get a realistic picture and we shall monitor the price and flow evolution.

There is very high percentage of Vertical Integration between Exporters and Washing Station owners this season. Offtake and pre-finance agreements are in place allowing exporters to access coffee at farmgate level and bypassing the ECX altogether. Expectation are that an even smaller proportion of this crop will find its way to ECX compared to last season.

Focusing on exports, below we compare Export figures for the current crop vs past 2 crops. We have started the “year” in May to try to outstrip the overlap between one crop and another, we could have started 2 month earlier at the start of the seasonal increase in shipments, however we believe that March and April shipments usually include a high proportion of previous crop Naturals…

What we can derive from the last 2 years is that we should see a drop in shipment over the period September to December/January followed by an increase from February 21 onwards as New Crop starts to be exported. Whatever the case (and confirmed by ECX figures) the 19/20 crop is a very disappointing crop and even if ECX volumes pick up the coming weeks, export quantities are likely to remain on the lower side.

https://www.coffeeithaka.com/wp-content/uploads/2020/08/ithakaDSC01909.jpg12001800Charles Seara Cardosohttps://www.coffeeithaka.com/wp-content/uploads/2020/08/logo-ithaka_350133.pngCharles Seara Cardoso2020-10-16 15:39:112020-10-16 17:43:34Washing Stations open throughout

The weather has changed for the better in Ethiopia in recent days. It is drier and these conditions are more favourable for ripening and drying after picking. Additionally, roads that were impassable for weeks because of wet weather conditions have now become operational; we expect more coffee to move from upcountry to ECX warehouses, increasing the volumes available to exporters. Export business continues subdued and below last year’s volumes and we believe that this trend will continue for the remainder of the crop. Our initial thoughts on the size of the 2020/21 Djimmah Crop are positive, conditions have been favourable and we are expecting a good crop, higher than last year and, importantly, better quality.

Saudi Arabia which is the single largest buyer of Naturals from Ethiopia (Grades 4 and 5) have decreed that the maximum allowable number of defects that can be imported to Saudi is 26 defects, i.e. grade 3 quality; if this regulation is enforced it would have a big impact on the Ethiopia Natural Supply Chain, since the competition for better quality coffees would intensify. Furthermore much more raw coffee would be needed to achieve Grade 3 quality squeezing the price for grade 4 and 5 coffees, particularly in a year where quality is below average. Some exporters have told us that a few Saudi buyers have requested contracts to be changed from Grade 4 and 5 to 3. The price difference between a grade 3 and a grade 4 is much more significant than a 4 to a 5. It remains to be seen if this regulation is enforced in the coming weeks and months.

Daily positive Covid tests are just under 1,000 for the past few days. The total number of positive cases has reached 82 k.