The Coffee and Tea Authority (C&TA) this week decreased hugely the Minimum Registration prices by around 20 c/lb while NY increased 8 cents week on week. We are not sure why this happened since last week registrations surely increased as shippers took advantage of a higher NY (the highest since the collapse that followed the invasion of Ukraine). Shippers continue to offer coffee at same levels as a week ago (around 200 c/lb for Grade 5) but with NY lower buyers have shied away a little this week. Upcountry agrabes are offering Grade 5 at equivalent of 210 c/lb FOB. Washed coffee offers continue firm, Grade 2 from the South (Sidamo and Yirgacheffe) at >+100 FOB. Limu 2 at +50 FOB. Buyers are hard to comeby at these steep differentials but some business is taking place.

It has started raining, as expected, in recent days, helping to ripen the crop on the tree. The rains should continue until the start of the harvest in October. A less desirable consequence of the rainy weather are impassable roads, frustrating agrabes and shippers as they try to move coffee from the growing areas to Addis Ababa for processing and onwards for export.

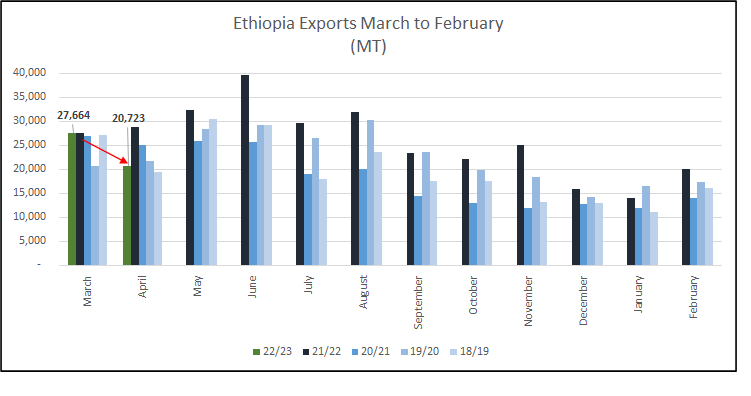

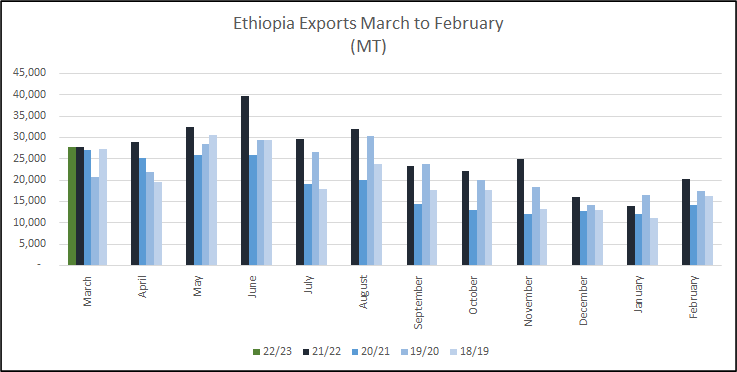

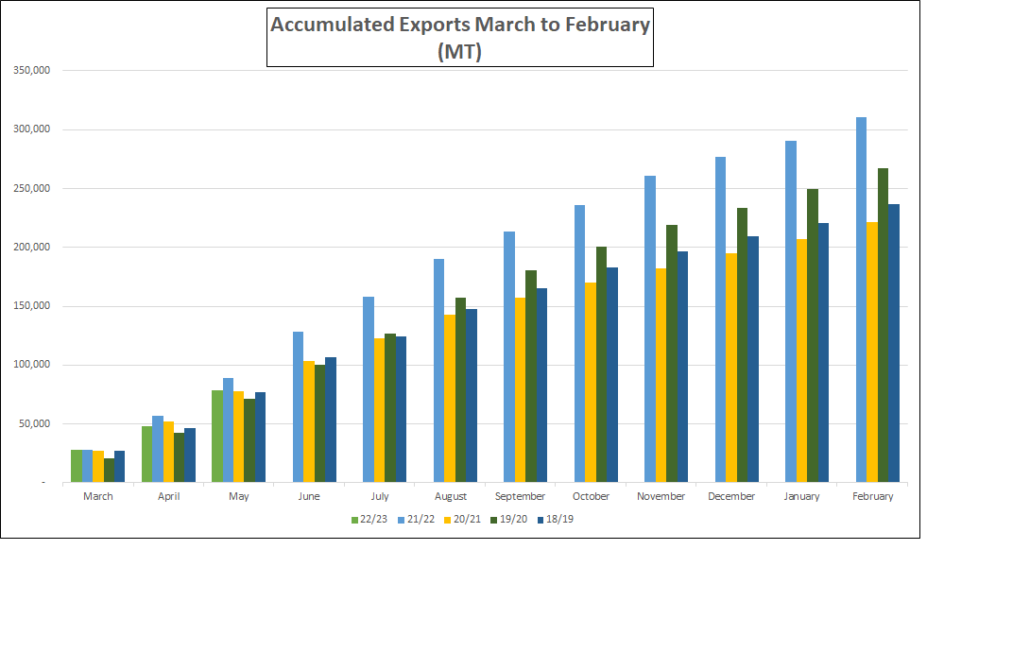

May exports recovered some of the lost ground following a disappointing April; The 2022 M/A/M quarter is the second highest M/A/M in the past 5 years, 2021 was a truly exceptional year. 2022 M/A/M Exports are at 78 K MT (May 2022 exports 30 K MT have only been bettered in the last 5 years by May 2021), we seem to be well on our way to reach 270 K MT possibly even 300 K MT exports March 22 to February 23, we shall see what the next 9 months have instore for us!

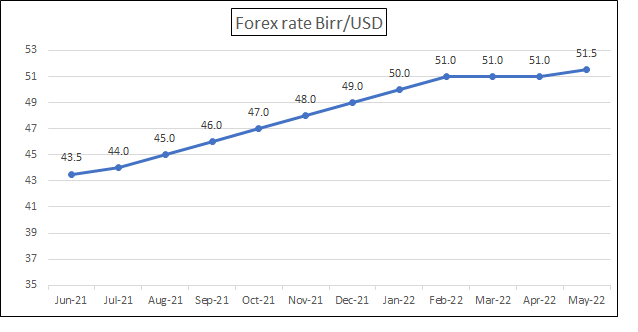

Birr 51.69 = USD 1

In other news, Beverages Multinational Coca-Cola Beverages Africa is to invest USD 100 M in a bottling plant in Ethiopia, increasing production and adding 500 people to the workforce. Perhaps the most significant aspect of this investment is that it shows that foreign investors are feeling confident that the current stalemate in hostilities between the army and rebels groups opposed to the Central Government will prevail.

Have a good weekend